As we reach the midpoint of 2024, the Commercial Real Estate (CRE) market continues to exhibit diverse trends across different sectors. Here’s a detailed analysis of the current state of the office, retail, and industrial markets, shedding light on the challenges and opportunities that lie ahead.

Office Sector

The office sector remains under pressure, with net absorption still in negative territory, indicating that more office space is being vacated than leased. However, there are emerging signs of improvement.

Office Sector

The office sector remains under pressure, with net absorption still in negative territory, indicating that more office space is being vacated than leased. However, there are emerging signs of improvement.

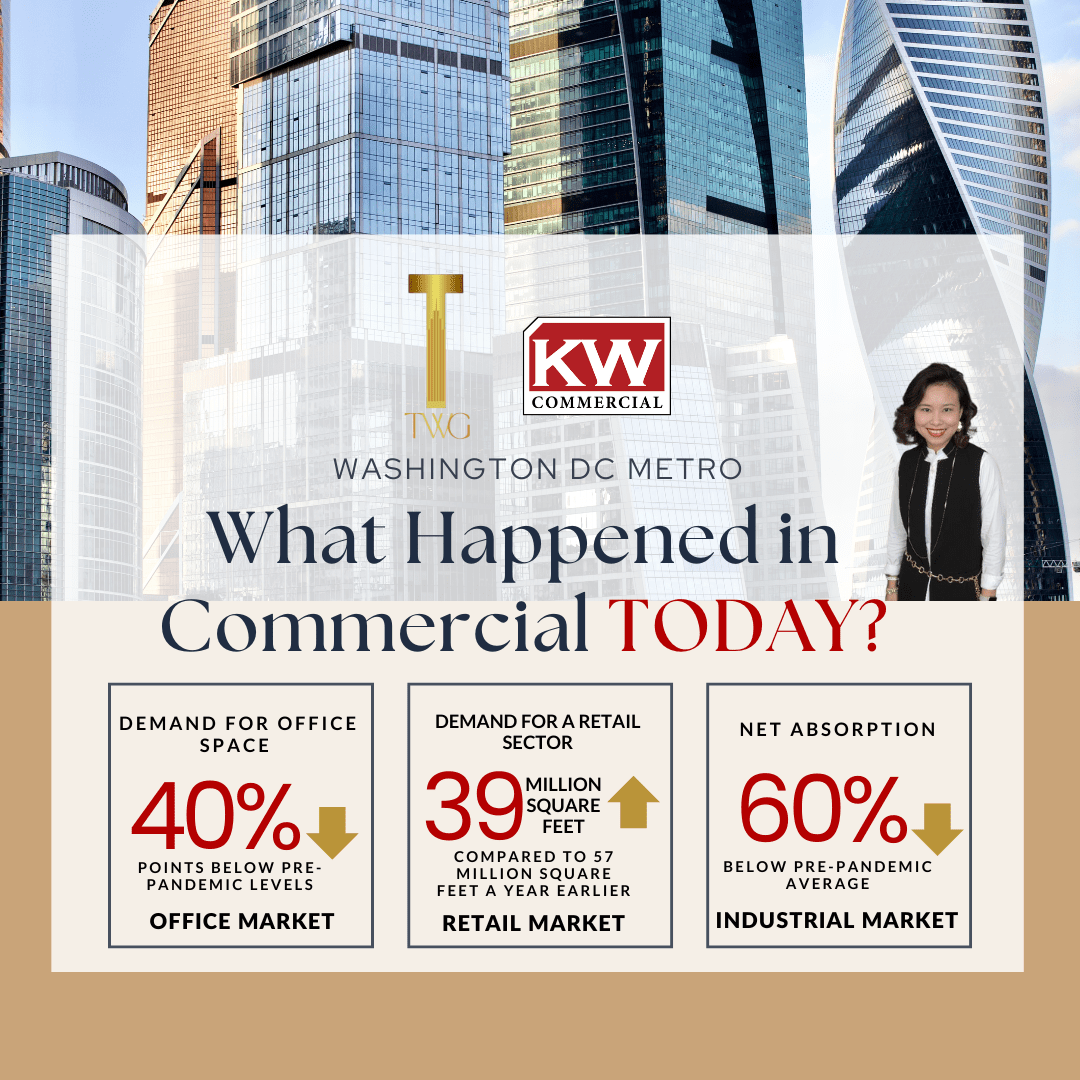

- Narrowing Gap: As of May 2024, the gap between vacated and occupied office spaces has narrowed, with 49 million square feet of space vacated more than leased. This is a significant reduction from 57 million square feet in Q1 2024 and 59 million square feet at the end of 2023.

- Leasing Activity: While there may be a slight increase in demand for office space in 2024, the overall outlook remains cautious. Leasing activity, a key indicator of tenant demand and interest, is still around 40% points below pre-pandemic levels, reflecting ongoing hesitancy among potential tenants.

The road to recovery for the office sector is likely to be gradual. Efforts to adapt office spaces to new hybrid work models and enhancing their appeal will be critical in driving future demand.

Retail Sector

The retail sector is experiencing unprecedented tightness in availability conditions, highlighting a robust demand despite limited supply.

Retail Sector

The retail sector is experiencing unprecedented tightness in availability conditions, highlighting a robust demand despite limited supply.

- Record-Low Availability: Only 4.7% of retail space is currently available for lease, marking the lowest level on record. The vacancy rate remains near 4%, reflecting sustained demand.

- Increased Absorption: Over the past 12 months, demand for retail spaces has surged, with net absorption increasing by nearly 39 million square feet compared to 57 million square feet a year earlier.

- Future Outlook: With fewer new construction projects in the pipeline, the fundamentals of the retail sector are expected to remain tight throughout 2024. Retail spaces, particularly in prime locations, are likely to continue experiencing high demand.

This tight market presents both challenges and opportunities for retailers and landlords. Strategic positioning and innovative leasing strategies will be essential to navigate this competitive landscape.

Industrial Sector

After a period of robust growth driven by the e-commerce boom, the industrial sector is now facing a slowdown.

Industrial Sector

After a period of robust growth driven by the e-commerce boom, the industrial sector is now facing a slowdown.

- Decline in Net Absorption: Net absorption levels have plummeted, reaching lows not seen in over a decade. Currently, net absorption is 68% lower than a year ago and 60% below the pre-pandemic average.

- Changing Consumer Behavior: High borrowing costs and shifting consumer preferences from goods to services have impacted demand for industrial spaces.

- Future Prospects: The outlook for the industrial sector suggests continued softening. Adapting to these changes by repurposing spaces and targeting emerging industries could provide pathways to mitigate the decline.

The industrial sector’s future hinges on its ability to adapt to changing market conditions and evolving consumer behaviors. Flexibility and innovation will be key to sustaining demand.